Research

March 13, 2026

GDP

U.S. economy grew even slower than originally estimated in Q4, up just 0.7% at annual rate

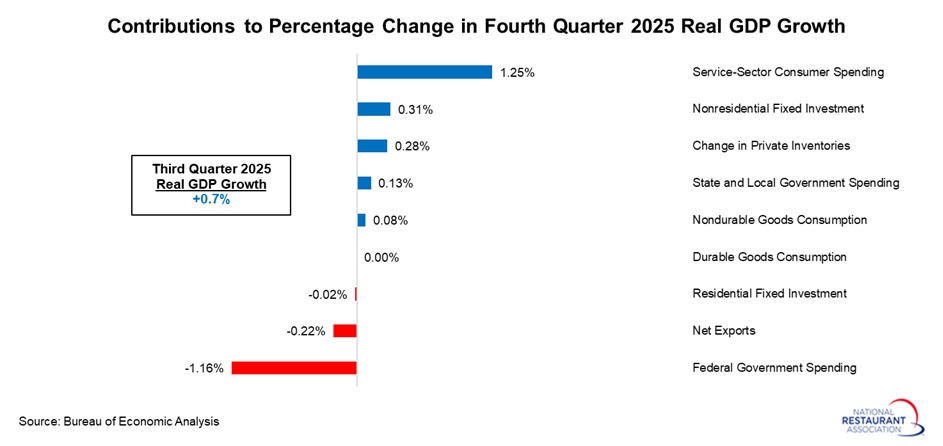

U.S. economic growth slowed sharply in the fourth quarter, rising just 0.7% at an annual rate—half the pace previously estimated and a steep drop from 4.4% in the third quarter. The federal government shutdown was the primary drag, subtracting an estimated 1.16 percentage points from headline GDP. In addition, updated data point to softer service‑sector spending and weaker business investment than initially reported, contributing to the downward revision.

Total consumer spending and fixed investment, a proxy for domestic demand, rose 1.9% at an annual rate in the fourth quarter, easing from 2.9% in the prior quarter. That is a decent rate of growth, albeit one that is softer than desired.

Looking ahead, the National Restaurant Association expects the economy to continue expanding, with real GDP projected to grow 2.4% in 2026. Even so, several risks could weigh on the outlook, including rising energy costs and heightened geopolitical uncertainty. The coming weeks will be important in determining how significantly these downside pressures might temper growth and potentially offset some of the policy-driven tailwinds expected to support momentum this year.

Digging deeper into the data, consumer spending remained uneven, with solid gains in services (+2.7% at an annual rate) offset by essentially flat demand for goods. Overall, personal consumption expenditures rose 2.0% in Q4, down from 3.5% in Q3, contributing 1.33 percentage points to headline GDP. Even so, spending at foodservices and accommodations subtracted 0.05 percentage points from GDP in Q4, pulling back after contributing positively in each of the previous two quarters.

Investment activity rebounded in Q4, rising 3.3% at an annual rate after being flat in Q3. Fixed investment strengthened from 0.8% growth in Q3 to 1.6% in Q4, but with nonresidential fixed investment easing from 3.2% to 2.2%. Equipment (+3.9%) and intellectual property products (+5.7%) both performed well, while structures investment (‑7.1%) declined for the eighth consecutive quarter. Meanwhile, residential investment (‑0.5%) fell for the fourth straight quarter, and businesses modestly rebuilt inventories after drawing them down over the prior two quarters.

Net exports subtracted 0.22 percentage points to real GDP in Q4, pulling back somewhat after robust gains in Q2 and Q3. Both exports (-3.3% at an annual rate) and imports (‑1.1%) were lower in the latest quarter.

Federal government spending was the largest drag on growth, with federal outlays falling at an annualized pace of 16.7% and subtracting 1.16 percentage points from GDP in Q4—an impact driven entirely by the federal government shutdown. In contrast, state and local government spending rose 1.2% in Q4, adding 0.13 percentage points to top‑line real GDP growth.

Total consumer spending and fixed investment, a proxy for domestic demand, rose 1.9% at an annual rate in the fourth quarter, easing from 2.9% in the prior quarter. That is a decent rate of growth, albeit one that is softer than desired.

Looking ahead, the National Restaurant Association expects the economy to continue expanding, with real GDP projected to grow 2.4% in 2026. Even so, several risks could weigh on the outlook, including rising energy costs and heightened geopolitical uncertainty. The coming weeks will be important in determining how significantly these downside pressures might temper growth and potentially offset some of the policy-driven tailwinds expected to support momentum this year.

Digging deeper into the data, consumer spending remained uneven, with solid gains in services (+2.7% at an annual rate) offset by essentially flat demand for goods. Overall, personal consumption expenditures rose 2.0% in Q4, down from 3.5% in Q3, contributing 1.33 percentage points to headline GDP. Even so, spending at foodservices and accommodations subtracted 0.05 percentage points from GDP in Q4, pulling back after contributing positively in each of the previous two quarters.

Investment activity rebounded in Q4, rising 3.3% at an annual rate after being flat in Q3. Fixed investment strengthened from 0.8% growth in Q3 to 1.6% in Q4, but with nonresidential fixed investment easing from 3.2% to 2.2%. Equipment (+3.9%) and intellectual property products (+5.7%) both performed well, while structures investment (‑7.1%) declined for the eighth consecutive quarter. Meanwhile, residential investment (‑0.5%) fell for the fourth straight quarter, and businesses modestly rebuilt inventories after drawing them down over the prior two quarters.

Net exports subtracted 0.22 percentage points to real GDP in Q4, pulling back somewhat after robust gains in Q2 and Q3. Both exports (-3.3% at an annual rate) and imports (‑1.1%) were lower in the latest quarter.

Federal government spending was the largest drag on growth, with federal outlays falling at an annualized pace of 16.7% and subtracting 1.16 percentage points from GDP in Q4—an impact driven entirely by the federal government shutdown. In contrast, state and local government spending rose 1.2% in Q4, adding 0.13 percentage points to top‑line real GDP growth.

.jpg?lang=en-US "contributions-to-real-GDP-growth-(1).jpg")