Research

June 17, 2026

Monetary Policy

Federal Reserve leaves rates unchanged but with a possible rate hike later in 2026

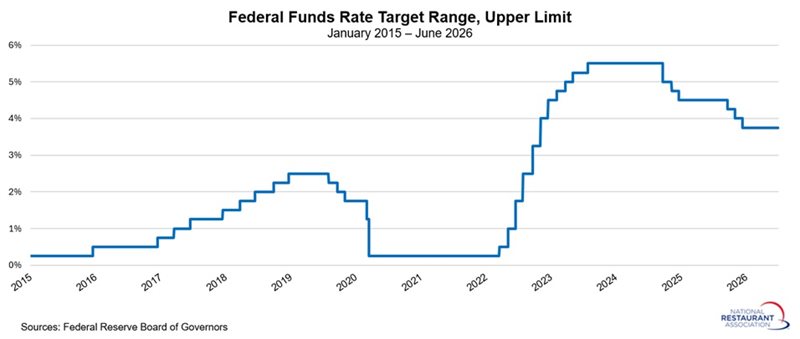

At its June 16–17 meeting, the Federal Open Market Committee (FOMC) left short-term interest rates unchanged, marking the fourth consecutive meeting without a policy move following three straight 25-basis-point cuts at the end of 2025. The federal funds rate remains in a target range of 3.50% to 3.75%.

The meeting was also notable as the first chaired by Kevin M. Warsh. Unlike the prior gathering, the decision drew no dissents.

More importantly, updated economic projections signaled a potential shift in policy direction. The FOMC now anticipates one rate increase later this year and projects PCE inflation to reach 3.6%. After several meetings focused on the timing of rate cuts, this pivot toward a possible hike reflects mounting inflationary pressures.

The FOMC underscored this concern in its statement: “Inflation remains elevated relative to the Committee's 2 percent goal, in part reflecting supply shocks that have driven price increases in certain sectors, including energy. The Committee is committed to restoring price stability.” Given that price growth has trended higher so far this year, a more hawkish tone on inflation is not surprising. The current projection is also for one cut in 2027. It is important to note that this is a static projection, and with incoming data, the future direction of monetary policy might change. For the foreseeable future, interest rates are likely to remain unchanged, giving the FOMC time to adjust to what happens in the economy before making any change in interest rates.

At the same time, the Committee highlighted a number of positives in the broader economy, noting that “economic activity is expanding at a solid pace despite elevated uncertainty that owes, in part, to the conflict in the Middle East. Productivity growth and capital investment are strong. Job gains have kept pace with the workforce, and the unemployment rate has changed little.”

Consistent with that assessment, the U.S. economy remains resilient. The median forecast calls for real GDP growth of 2.2% this year, with the unemployment rate expected to edge up modestly to 4.3%.

For the restaurant industry, elevated interest rates continue to pressure borrowing costs, often slowing expansion, renovations, and other capital investments. A higher-rate environment—should it materialize later this year—could further increase credit burdens, dampen consumer spending, and potentially constrain demand in sectors highly sensitive to discretionary income, including foodservice and hospitality.

The meeting was also notable as the first chaired by Kevin M. Warsh. Unlike the prior gathering, the decision drew no dissents.

More importantly, updated economic projections signaled a potential shift in policy direction. The FOMC now anticipates one rate increase later this year and projects PCE inflation to reach 3.6%. After several meetings focused on the timing of rate cuts, this pivot toward a possible hike reflects mounting inflationary pressures.

The FOMC underscored this concern in its statement: “Inflation remains elevated relative to the Committee's 2 percent goal, in part reflecting supply shocks that have driven price increases in certain sectors, including energy. The Committee is committed to restoring price stability.” Given that price growth has trended higher so far this year, a more hawkish tone on inflation is not surprising. The current projection is also for one cut in 2027. It is important to note that this is a static projection, and with incoming data, the future direction of monetary policy might change. For the foreseeable future, interest rates are likely to remain unchanged, giving the FOMC time to adjust to what happens in the economy before making any change in interest rates.

At the same time, the Committee highlighted a number of positives in the broader economy, noting that “economic activity is expanding at a solid pace despite elevated uncertainty that owes, in part, to the conflict in the Middle East. Productivity growth and capital investment are strong. Job gains have kept pace with the workforce, and the unemployment rate has changed little.”

Consistent with that assessment, the U.S. economy remains resilient. The median forecast calls for real GDP growth of 2.2% this year, with the unemployment rate expected to edge up modestly to 4.3%.

For the restaurant industry, elevated interest rates continue to pressure borrowing costs, often slowing expansion, renovations, and other capital investments. A higher-rate environment—should it materialize later this year—could further increase credit burdens, dampen consumer spending, and potentially constrain demand in sectors highly sensitive to discretionary income, including foodservice and hospitality.